Solutions

Markets

References

Company

Profile

Partners

Contact

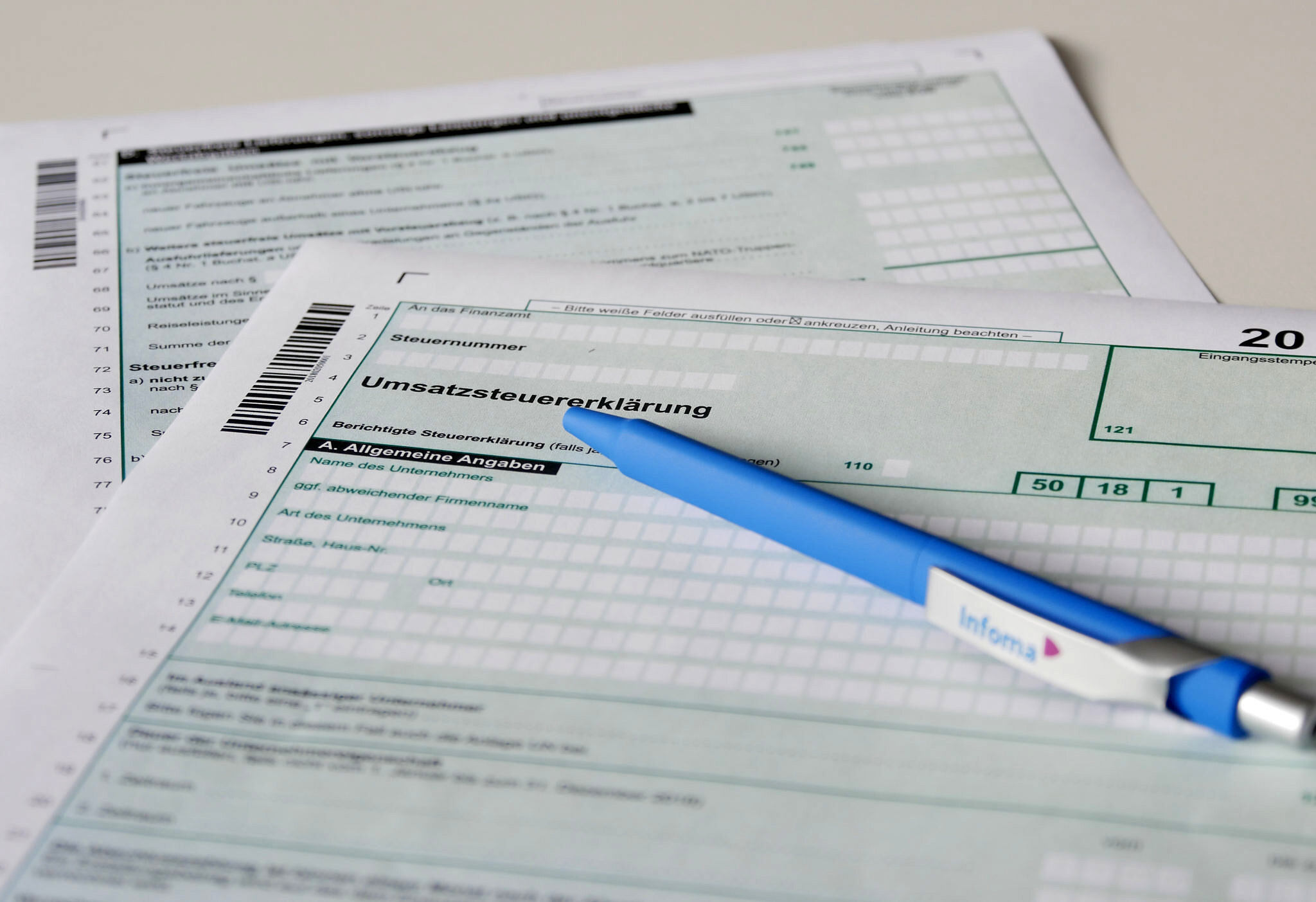

New VAT regulation challenges local governments and churches

A new rule is affecting the economic actions of local governments and churches: Areas that in the past faced no VAT will now be subject to it. The new regulation is Sec. 2b of the VAT Act.

In addition to the new regulation of Sec. 2b VAT Act and changes in the 2015 annual tax act, the elimination of Sec. 3 para. 3 VAT Act has removed the link to the corporate tax. Under the new regulations, legal persons under public law must make market-relevant, private law payments according to the same basic principles as other market participants. Payments made on a public law basis (such as articles of association and/or administrative acts) but not subject to a general foreclosure, may be subject to taxation in the future.

The new regulation came into force on 1/1/2017. By adding Sec. 27 para. 22 VAT Act, the legislature also provided the opportunity to opt to submit a one-time declaration to the tax authorities by 12/31/2016 and continue complying with the regulations of sec. 2 para. 3 VAT Act in the version dated 12/31/2015. The declaration needed to be submitted one time for all payments made before 1/1/2021. By doing so, legal persons under public law can determine the more beneficial legal position for them during the transitional period. The new VAT Act regulations apply without exception after 1/1/2021 for all taxable payments.

Therefore, we recommend that our customers consider these issues early on; researching and reviewing all contracts can take quite some time. In addition, it is important to establish the necessary expertise in your local government or church.

We offer support in implementing the new guidelines with our solution Infoma newsystem central contract administration, as well as through our consulting services. The integrated module provides efficient contract management with centralized or decentralized updates and collects all contracts into a central directory, giving an overview of amounts to be paid, documents associated with the contract, and upcoming deadlines. The advantage: Contractual data is centrally available, with the option of decentralized administration, e.g. in departments.

Our goal is for our customers to understand the topic of VAT and the associated responsibilities. Errors related to VAT can, after all, have wide-ranging consequences.

Contact

Contact